Strategic Fundraise

Digital Assets • Stablecoins • Onramps • Offramps • Identity • Network

Jan 14th, 2026

Bank Linking Stack • ACH • Data Connectivity

The FinTech Developer Guide: Understanding the ACH SystemDecember 9th, 2022 | 10 mins

Whether you're a seasoned professional or a curious consumer, understanding the ACH system is crucial to navigating and understanding electronic payments. In this article, we'll dive deeper into ACH transactions and systems and understand how developers can offer this payment method to their customers.

ACH is an electronic network that facilitates the exchange of financial transactions, such as direct deposits, bill payments, and fund transfers, among participating banks and financial institutions within the United States. It is operated by the National Automated Clearing House Association (NACHA) and regulated by the Federal Reserve and the Electronic Payments Network.

ACH transactions can be broadly categorized into two types: ACH Credits and ACH Debits. ACH Credits are transactions where funds are pushed into a recipient's account, such as direct deposit of paychecks, government benefits, or tax refunds. ACH Debits involve pulling funds from an account to make payments or transferring money to another account. Both types of transactions offer a convenient, secure, and cost-effective way to move money electronically.

1. Cost Efficient

ACH transactions are typically less expensive than other electronic payment methods, such as wire transfers and credit card transactions.

2. Security

The Federal Reserve and the Electronic Payments Network regulate the system, ensuring that stringent security measures are in place to protect sensitive information and prevent unauthorized access.

3. Convenience and Ease

With ACH, funds can be transferred seamlessly and electronically, eliminating the need for paper checks and manual processing.

1. Slower processing times

ACH transactions typically take one to two business days to process.

2. Increased risk of fraud

The large volume of electronic transactions passing through the system makes it an attractive target for fraudsters. Like other payment methods, individuals may target users through phishing to gain unauthorized access to sensitive information.

3. Limitations on international transfers

The ACH network primarily facilitates domestic transactions within the United States. Other payment methods or specialized services may be a better fit for those who require international payment capabilities.

Overall, ACH transactions offer an efficient, secure, and convenient way to manage and move money in our increasingly digital world, making them an essential part of the modern financial ecosystem. By understanding the potential drawbacks and taking appropriate measures to mitigate risks, developers can benefit from the many advantages ACH transactions offer.

Some of the most common use cases for ACH include:

1. Direct deposits

Users can receive their salaries or other payments directly into their bank accounts without needing paper checks.

2. Bill payments

Bill payments made through fintech apps often utilize ACH to facilitate the transaction, streamlining the process and allowing users to manage their finances more efficiently.

3. Peer-to-Peer payments

Peer-to-peer payments enable individuals to send and receive money seamlessly through digital platforms, making it easier to split expenses, repay debts, or transfer funds between friends and family members.

Creating ACH transactions necessitates specific information, such as a customer's bank account and routing number, as well as their full name and address. This data is crucial for the creation and processing of ACH transactions, regardless of whether they are debits or credits, and is used to authenticate and validate customer data in order to mitigate fraud risks.

In the past, getting a customer to connect their accounts or provide the above data was a cumbersome task. However, this process has become more streamlined thanks to bank linking aggregators like Plaid, Finicity, MX and etc. Retrieving Consumer Permissioned ( a.k.a User Permissioned) Financial Data with aggregators has made supporting ACH infinitely simpler.

While bank linking aggregators have streamlined a tedious task, it still leaves developers with challenges such as incomplete financial institution coverage and having to manage multiple integrations in house. That's where Meld comes in!

We've simplified integrating and managing multiple bank linking aggregators with a single integration and out-of-the-box UI. Meld enables developers to get the benefits of integrating with numerous providers for the work of one. We help maximize institution coverage and reduce connection error rates. Learn how our smart routing driven by our network data and AI models, increase conversion rate to bank account connection by over 55%.

Learn more about the challenges of making bank linking work and how Meld helps here.

As the fintech industry continues to grow and innovate, ACH remains a valuable tool for developers looking to build cutting-edge applications that cater to the evolving needs of businesses and consumers. Meld has made implementing lower fraud ACH across fintech products much easier and more accessible.

Learn more on how to scale with Meld here.

Q: What does ACH stand for?

ACH stands for Automated Clearing House and is an electronic network that facilitates financial transactions among participating banks and financial institutions within the United States.

Q: What is the meaning of ACH in the context of financial transactions?

ACH refers to a payment system that enables the secure and efficient exchange of financial transactions, such as direct deposits, bill payments, and fund transfers, electronically between participating banks and financial institutions.

Q: What is an ACH payment?

An ACH payment is an electronic transfer of funds between banks and financial institutions through the Automated Clearing House network. ACH payments include transactions like direct deposits, bill payments, and peer-to-peer transfers, offering a cost-effective and convenient way to move money electronically.

Q: What is the purpose of the ACH system?

The purpose of the ACH system is to provide a reliable, secure, and efficient method for processing financial transactions electronically within the United States. ACH transactions play a pivotal role in the daily functioning of the economy, connecting businesses, consumers, and financial institutions and reducing the need for paper checks and manual processing.

Strategic Fundraise

Digital Assets • Stablecoins • Onramps • Offramps • Identity • Network

Jan 14th, 2026

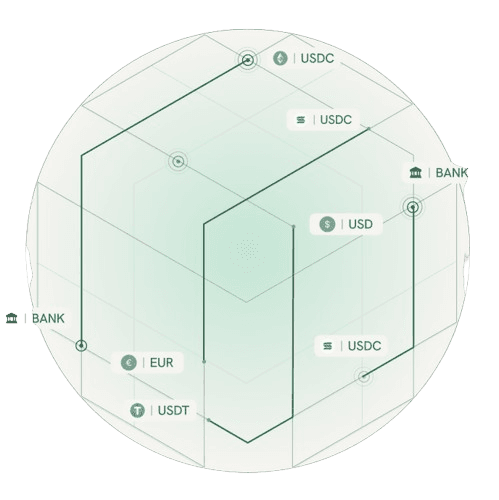

Introducing Meld Network: Access Digital Assets Anywhere

Digital Assets • Stablecoins • Identity • Network

Nov 18th, 2025

Meld Partners with Phantom to Enhance Global Crypto Access

Aug 19th, 2024