Strategic Fundraise

Digital Assets • Stablecoins • Onramps • Offramps • Identity • Network

Jan 14th, 2026

Bank Linking Stack • Fraud Prevention • Data Connectivity

The FinTech Developer Guide: Using Bank Linking Data Aggregators To Fight FraudApril 13th, 2023 | 8 mins

As the fintech industry continues to grow and evolve, ensuring robust security measures is paramount. Fraud prevention is a critical concern for fintech developers, as they handle sensitive financial data. One powerful tool in their arsenal is bank linking data aggregators. In this blog post, we will explore how these aggregators can effectively combat fraud, safeguard customer information, and enhance security for fintech developers and their users.

Bank linking data aggregators act as intermediaries between fintech platforms and financial institutions, streamlining the process of accessing and consolidating financial data. By integrating with multiple banks and financial service providers, these aggregators retrieve transactional and account data from various sources in a standardized format. This comprehensive data aggregation is instrumental in identifying patterns and anomalies that could indicate fraudulent activity, offering developers greater visibility into their users' financial behavior.

Data aggregators continuously monitor transactional data in real-time, enabling swift detection and prevention of fraudulent activities. By analyzing user spending patterns, location data, and transaction history, these aggregators can identify suspicious transactions or unusual account behavior. This allows fintech developers to implement proactive security measures, such as two-factor authentication, transaction verification, and risk-based alerts. Real-time fraud monitoring helps prevent fraudulent transactions before they cause substantial damage, protecting both users and the platform itself.

Bank linking data aggregators employ advanced algorithms and machine learning techniques to assess the risk associated with individual transactions and user behavior. By analyzing vast amounts of data, including spending habits, income sources, and account balances, these aggregators create a risk profile for each user. Any deviation from established patterns triggers risk alerts, allowing fintech developers to take appropriate action promptly. This proactive approach not only prevents fraudulent activities but also reduces false positives, ensuring a seamless user experience without unnecessary disruptions.

Bank linking data aggregators enhance security by providing multi-factor authentication capabilities to fintech developers. By leveraging the data obtained from various financial institutions, these aggregators can offer stronger authentication methods beyond traditional username-password combinations. This may include biometric authentication, device recognition, or one-time password (OTP) verification. Multi-factor authentication significantly reduces the risk of unauthorized access and protects sensitive user information from being compromised.

Fintech developers face stringent regulatory requirements, such as Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. Bank linking data aggregators help ensure compliance by securely collecting and verifying customer information from multiple financial institutions. This streamlines the onboarding process, minimizing the risk of fraudulent accounts or identity theft. The aggregators' adherence to industry best practices and compliance standards ensures that fintech platforms maintain the necessary security measures, protecting both the developer and their users from potential legal and financial repercussions.

While bank-linking data aggregators help developers easily access Consumer Permissioned Data, there are still other challenges to consider - one of the key hurdles is that no aggregator offers complete coverage. To get full coverage and support all banks and financial institutions, developers must work with and build integrations into multiple providers. However, institution coverage changes daily, and it isn't clear which set of providers a developer can rely on for consistent and complete coverage.

That's where Meld comes in! We help you manage your multi-vendor fintech stacks with just a single integration. With just a few lines of code, developers can access over 13,000+ banks and financial institutions in the U.S. and Canada alone. Meld's Bank Linking Stack gives developers the benefits of integrating with numerous providers for the work of one. We help maximize institution coverage and reduce connection error rates. With broader coverage, you can rest assured that you can connect to your customer's bank account and securely access the Consumer Permissioned Data you need to verify their identity accurately and efficiently. An increase in coverage helps boost conversion rates while creating redundancy across institutions and minimizes churn with Meld.

Want to learn more about how Meld is making Bank Linking work? Read here to learn more!

Fraud prevention is a top priority for fintech developers, and bank linking data aggregators play a pivotal role in combating fraudulent activities. Through comprehensive data aggregation, real-time fraud monitoring, advanced risk assessment, multi-factor authentication, and regulatory compliance support, these aggregators provide robust security measures. By integrating with these aggregators, fintech developers can bolster their platform's security, protect user data, and foster trust among their user base. As the fintech industry continues to thrive, harnessing the power of bank linking data aggregators is crucial for staying ahead in the fight against fraud and ensuring a safe and secure financial ecosystem.

Ready to take your fintech integrations to the next level? Discover how Meld can revolutionize the way you manage your bank linking stack so you can build robust consumer experiences across ACH and bank-to-bank payments, personal finance, identity verification underwriting, and more here.

Q: What is KYC, and why is it important in the fintech industry?

KYC, or Know Your Customer, is the mandatory process of verifying the identity of customers to assess their risk profile and ensure regulatory compliance. It plays a crucial role in fintech by preventing fraud, identity theft, and money laundering while maintaining customer trust and confidence.

Q: What does the term 'User Permissioned Data' mean?

User Permissioned Data, or Consumer Permissioned Data, refers to the financial and personal information that customers voluntarily share with fintech companies. This data enables a more comprehensive assessment of a customer's identity and risk profile, enhancing the KYC process.

Q: Who are account aggregation providers, and what role do they play in KYC?

Account aggregation providers, often called data aggregators, collect and consolidate financial data from multiple sources, such as banks and financial institutions. They play a vital role in KYC by providing fintech companies access to customer information, which helps streamline identity verification and risk assessment processes.

Q: How do data aggregators help improve the KYC process?

Data aggregators, also known as bank-linking data aggregators, help improve the KYC process by securely accessing and consolidating customer data from various sources. This information enables fintech companies to cross-reference and verify a customer's identity more accurately and efficiently, ultimately enhancing security and compliance.

Q: What distinguishes financial aggregators from other types of data aggregators?

Financial aggregators specifically focus on collecting and consolidating data from banks and financial institutions. They are instrumental in streamlining the KYC process in fintech, as they provide companies with critical information for accurate identity verification and risk assessment.

Q: How can data aggregation companies enhance the security and compliance of fintech businesses?

Data aggregation companies help fintech businesses enhance security and compliance by providing access to comprehensive and up-to-date customer information. This data enables companies to make well-informed decisions, mitigate risks, and maintain compliance with KYC regulations, ultimately safeguarding their assets and customer trust.

Strategic Fundraise

Digital Assets • Stablecoins • Onramps • Offramps • Identity • Network

Jan 14th, 2026

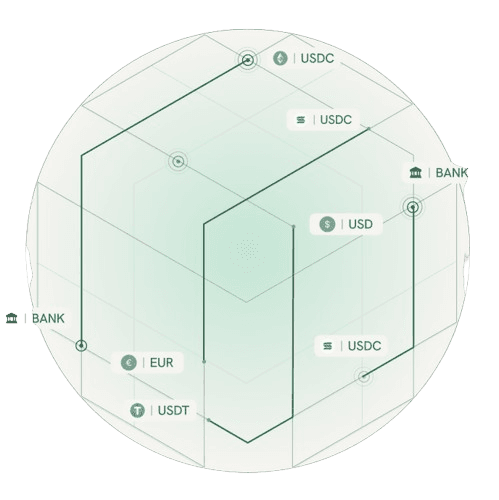

Introducing Meld Network: Access Digital Assets Anywhere

Digital Assets • Stablecoins • Identity • Network

Nov 18th, 2025

Meld Partners with Phantom to Enhance Global Crypto Access

Aug 19th, 2024